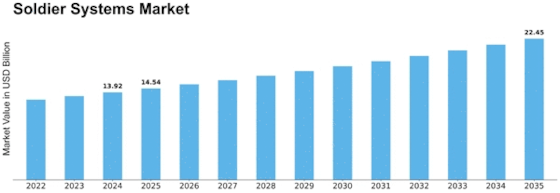

Industry Overview

The soldier systems market structure is defined not only by product and technology segments, but also by its end-users (military, law enforcement, civil defence) and the functional capabilities (surveillance, combat support, logistics support) embedded in the systems. According to MRFR, the global market stood at USD 12.76 billion in 2022, projected to grow to USD 19.7 billion by 2032 (CAGR 4.44%).

Market Outlook

The functional segmentation is sharpening: surveillance, combat support and logistics support capabilities are increasingly integrated into soldier systems. MRFR notes that surveillance (real-time information), combat support (equipment enabling missions) and logistics support (supply-chain, sustainment) are key functional segments. End-users beyond the traditional military—such as law enforcement agencies and civil defence organisations—are adopting advanced soldier systems for border security, counter-terrorism and disaster response. This broadening of user base is expanding the market’s reach and complexity.

Key Players

Companies such as Rheinmetall AG, Thales Group, Lockheed Martin Corporation, General Dynamics Corporation and SAAB AB are active across these functional domains, offering systems that span wearable equipment, sensors, communications and support kits. These players are increasingly building modular platforms that can be customised for specific end-users, from infantry to special forces to civil defence.

Segmentation Growth

- End-User: Military remains the largest category, but Law Enforcement and Civil Defence are growing. The MRFR report emphasises this shift.

- Functionality: Surveillance and combat support segments are growing rapidly, driven by requirements for situational awareness and mission-support capabilities. Logistics support, though less visible, is increasingly important in sustaining soldier systems operational readiness.

- Technology & Product: The enablement of functionality (surveillance, combat support) relies on wearable sensors, communication systems, advanced materials and integrated kits — looping back into the core segments.

This segmentation insight helps companies align product development to end-user and functionality priorities.

Conclusion

For content with an operational-focus (soldier readiness, mission support), emphasising functionality and end-user segmentation offers great value. The story is no longer just “gear for soldiers” but “systems for missions” — surveillance, combat operations, logistics sustainment. Companies that position their soldier systems as supporting entire mission cycles (not just equipment) will resonate deeply in defence communications.